I’m a little late to the party with Series I Savings Bonds (or I Bonds as they’re more typically called.)

I bonds were all the rage during the first months of 2022 and my wife and I each purchased I bonds back in April.

Ever since, I’ve found myself having to relearn how I bonds work and how to calculate their value.

To make it easy for myself the next time I inevitably forget some detail about I bonds, I wrote this post to explain exactly what I bonds are, as well as how and why you should purchase them.

What is an I bond?

I bonds are issued by the United States Department of the Treasury to raise money for the U.S. government.

The government might use this money to make up deficits in the federal budget or to fund infrastructure projects, among many other uses.

In short, when you buy an I bond, you’re loaning money to the US government. In turn, the US government promises to pay you back that money plus interest over a period of time.

Government bonds are “backed by the full faith and credit of the U.S. government”1 and so are considered a very safe investment—essentially risk-free.2

The neat thing about I bonds is that they’re tied to inflation, meaning that when inflation is high—as it is in 2022—I bonds pay a high interest rate.

What is the maturity of an I bond?

I bonds mature after 30 years.

If you buy an I bond on September 10, 2022, the bond will have an issue date of September 1, 2022 and a maturity date of September 1, 2052.

On September 1, 2052, you’d be paid your final month of interest and your principal would be returned, marking the end of life for this bond.

How is the interest rate of an I bond calculated?

The interest rate of an I bond has two parts, a fixed rate and an inflation rate.3

These two rates are joined to form the combined rate, which is the annual interest rate for the I bond.

What is the fixed rate for an I bond?

The fixed rate for an I bond is announced on May 1 and November 1 of every year.

Any I bond purchased between May 1 and October 31 will have the fixed rate announced on May 1, while any I bond purchased between November 1 and April 30 will have the fixed rate announced on November 1.

The fixed rate is called “fixed” because it never changes—the fixed rate at the time of purchase stays the same until the bond matures.

The fixed rate has been 0% since May 2020, though it has been as high as 3.60% in May of 2000.4

What is the inflation rate for an I bond?

The inflation rate, meanwhile, changes every 6 months based on changes in the Consumer Price Index for all Urban Consumers (CPI-U) for all items, including food and energy.

For example, in 2002, a dozen eggs cost $1. In 2022, a dozen eggs cost $2.90.

The CPI-U measures this change in price (i.e., inflation) not only for eggs, but for all the typical consumer goods and services, including food, clothes, cars, gasoline, electricity, rent, medical care, etc.

So if the CPI-U in May shows that, as a whole, the cost of these typical goods and services has increased by 10% over the previous six months, this would mean that:

- The cost of living has increased by 10%. In other words, if you were spending $100 a week six months ago, you’re now spending $110 a week for the same goods and services.5

- The inflation rate for any I bond purchased between May 1 and October 31 will be 20%, two times the semiannual inflation rate of 10%. This rate would last for six months, at which time it would change to the new inflation rate.

Like the fixed rate, the inflation rate is announced on May 1 and November 1 of every year.

The inflation rate was 9.62% in May 2022 (the highest it’s ever been) and has been as low as -5.56% in May 2009.4

(Yes, inflation rates can be negative. This is called deflation.)

What is the combined rate for an I bond?

The combined rate is essentially the fixed rate plus the inflation rate.

For the curious, the exact combined rate formula is fixed rate + (2 × semiannual inflation rate) + (fixed rate × semiannual inflation rate).

When the fixed rate is 0, as it has been for a while, the combined rate is simply the annual inflation rate.

The fixed rate is known when you purchase the bond and the inflation rate changes every May and November. Hence, the combined rate will also change every May and November.

For I bonds issued from May 2022 to October 2022, the fixed rate was 0% and the semiannual inflation rate was 4.81%.

To get the combined rate for these I bonds, we multiply the semiannual inflation rate by 2 to get the annual inflation rate of 9.62% and add the fixed rate of 0%, which comes out to 9.62%.

Sidenote

Combined rate = 0.00 + (2 × 0.0481) + (0.00 × 0.0481)

= 0.00 + 0.0962 + 0.00

= 0.0962 and 0.0962 × 100 = 9.62%

So until November rolls around and the inflation rate changes, these I bonds will pay an interest rate of 9.62%.

What happens if the inflation rate for an I bond is negative?

The combined rate for an I bond cannot go below zero.

As an example, I bonds issued from May 1, 2009 to October 31, 2009 had a semiannual inflation rate of -2.78% and a fixed rate of 0.10%.

Technically, the combined rate for these I bonds was -5.46%6, but since the combined rate can’t be negative, it was set to 0.

How is the inflation rate for an I bond calculated?

The inflation rate announced in May reflects the change in inflation from September of the previous year to March of the current year as measured by CPI-U.7

The inflation rate announced in November, meanwhile, reflects the change in inflation from March to September of the current year.

Sidenote

Why September to March?

The inflation rate for the I bonds released on May 1 needs to be calculated in April.

Since the CPI-U reading is released around the 10th of every month, however, the reading released in April is based on the data from March as April is still in progress.

So the most up-to-date CPI-U reading available in April reflects the prices collected in March.

Then if we go back six months from March, we arrive at September of the previous year as March 1 minus six months is September 1.

So we use the CPI-U from September (which was released in October) and the CPI-U from March (which was released in April) to calculate the semiannual inflation rate.

Hopefully that makes sense—this confused me for a good while.

Let’s take the 9.62% inflation rate announced in May 2022 as an example.

This inflation rate was determined by calculating the change in the CPI-U from September 2021 to March 2022.

The CPI-U in September 2021 was 274.310 and in March 2022 it was 287.504.8 And the percent change from 274.310 to 287.504 is 4.81%.9

This means the semiannual inflation rate was 4.81%.

To get the annual inflation rate, we multiply the semiannual inflation rate by 2, which gives us 9.62%.

When does an I bond pay interest?

The earned interest is added to the value of the bond on the first of each month.

So if you buy an I bond in March, you’ll receive the interest for March on April 1.

What is the best time to buy and sell an I bond?

Regardless whether you buy an I bond on the first or the last of the month, you’ll receive interest on the first of the following month.

Due to this, it’s preferable to have your money making interest in a savings account until the end of the month and then buy the I bond.

Conversely, you would want to sell an I bond early in the month after receiving that month’s interest.10

Do note, however, that it takes a few business days for an I bond purchase to go through, so give yourself some buffer.

When does an I bond’s interest compound?

An I bond’s interest is compounded semiannually.

So twice per year, the interest earned by the I bond during the previous 6 months is added to the principal value of the bond.

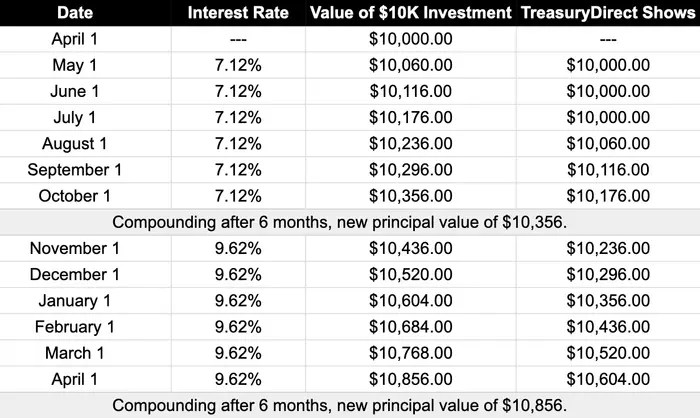

As an example, say you purchased a $10,000 I bond in April.

From May to October (May 1, June 1, July 1, August 1, September 1, and October 1), the monthly interest you’ll receive will be based on the original $10,000 purchase.

Let’s say that the interest rate during this time was 7.12%, which means the monthly interest added up to $356.

Starting on November 1, then, you’ll be paid interest on $10,356 (the new principal value of the bond) rather than on $10,000.

How do I purchase an I bond?

You can buy I bonds directly through TreasuryDirect.

Physician on FIRE has a great step-by-step guide on how to navigate the TreasuryDirect site to purchase I bonds.

What is the maximum amount of I bonds I can buy?

There is a limit of $10,000 per person, per calendar year.

So you can buy $10,000 worth of I bonds, your spouse can buy another $10,000, and you can buy $10,000 worth of I bonds for each of your kids.

There are two caveats to consider, however.

The first is that businesses or trusts technically count as another person. So if you have a business (or trust), that business can also buy $10,000 worth of I bonds.

The rule, then, is that one Social Security Number (i.e., a legal US resident) or Employer Identification Number (i.e., a business or a trust) can purchase a maximum of $10,000 worth of I bonds per calendar year.

The second caveat is that you can use your federal tax refund to purchase an extra $5,000 worth of I bonds.

So a family of four could potentially:

- Each buy $10,000 worth of I bonds

- Create a trust or business and buy another $10,000 worth of I bonds

- Purposely overpay on taxes to trigger a $5,000 refund and use this money to buy another $5,000 worth of I bonds

For a total of $55,000 worth of I bonds every year.

Is this worth the hassle? Likely not.

What is the minimum amount of I bonds I can buy?

The minimum denomination for I bonds is $25.11

So, every year, you can buy any amount of I bonds from $25 to $10,000, down to the penny.

For example, you can buy an I bond for $987.81 or $1,452.23—whatever floats your boat.

Can I sell an I bond?

Yes, after 12 months.12

So if you purchase an I bond in January 2022, you cannot sell it until January 2023.

The only other caveat is that if you sell an I bond before 5 years have passed, you lose the last 3 months of interest.

So if you purchase an I bond in January 2022 and sell it 18 months later in July 2023, you’ll only receive 15 months of interest.

If you instead wait five years until January 2027, you can sell the I bond penalty-free.

How do I see the value of my I bond?

- Login to your TreasuryDirect account.

- Click on Savings Bonds.

- Select Series I Savings Bonds and click Submit.

This video shows how to do this:

How do I calculate the value of an I bond?

To calculate the value of an I bond, we need to use the compound interest formula, P × (1 + r/n)nt, where p is the principal, r is the annual interest rate, n is the number of times the interest is compounded per year, and t is time in years.

For an I bond, n is 2 as it compounds semiannually.

For an example, take a look at the video above, which was recorded in mid-October 2022.

I bought $10,000 of I bonds in April 2022 and by mid-October I’d received 6 months of interest—May, June, July, August, September, and October.

The interest rate was 7.12% and since the bond is less than 5 years old, the last 3 months of interest aren’t included.13

Plugging in these numbers to the formula, we get $10,000 × (1 + 0.0712/2)2 × (6-3)/12, which equals $10,176.44.14

How do I calculate the exact value of an I bond?

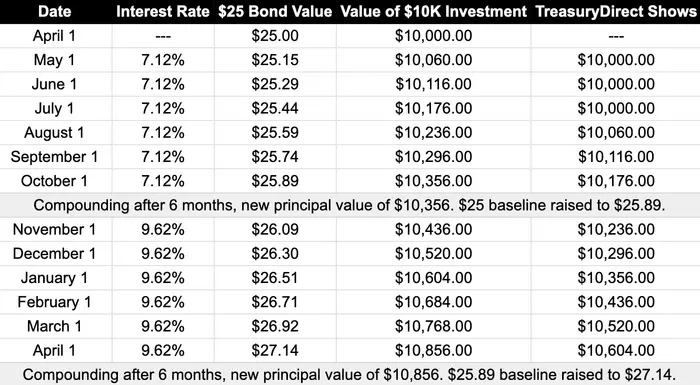

The eagle-eyed observer might have noticed that I calculated the bond’s value to be $10,176.44, while TreasuryDirect shows $10,176.

This post from TIPSWatch explains the discrepancy.

The catch is that all bond values are based on the $25 bond. This means that a $10,000 bond is worth 400 times what a $25 bond is worth.

So let’s run the same formula as above but using a $25 bond.

$25 × (1 + 0.0712/2)2 × (6-3)/12 = $25.44 and $25.44 × 400 = $10,176.

If you’re looking for a calculator to run these numbers for you, eyebonds.info is a wonderful tool for seeing an I bond’s growth in value over time.

How do taxes work for I bonds?

You do not pay any state or local taxes for I bonds, only federal tax.

And the federal tax can be deferred as you can choose whether to report I bond earnings annually or wait to report all the earnings when you sell the bond or the bond matures.

For example, say it’s January 2022, you’re working a full-time job, and you decide to buy a $10,000 I bond.

Additionally, let’s pretend that the combined rate for the I bond stays at 5% throughout 2022.

With this combined rate, you’d receive a bit more than $50015 in interest during 2022.

You could choose to report these $500 as earnings during 2022 and pay the corresponding taxes when you file in 2023.

Or you could wait.

Say you wait until January 2052 when the bond matures. Let’s pretend that by this time you’re retired and have $8,000 in earnings from your I bond.

As the bond has matured, you have no choice but to report the earnings.

Since you’re no longer working, however, your income is much lower. This puts you in a lower federal tax bracket and reduces the amount of tax you pay on the earnings.

And a final tax “trick” is to use I bond earnings to pay for qualifying education expenses, which makes the interest completely tax free.16

Should I buy an I bond?

The two big advantages of I bonds are that you can defer taxes and that they’re essentially risk free.

And now that inflation is high, a third advantage is the high interest rate—9.62% if you bought before October 31 and 6.89% if you bought after October 31.

The two disadvantages are that you can’t sell the I bond for a year and that you lose 3 months of interest if you sell before 5 years.

Personally, my wife and I each bought $10,000 of I bonds in April 2022 and will likely buy again in early 2023.

No other investment is offering such a high return and the stock market looks like it will remain highly volatile throughout 2023.

If you have the money sitting around in a savings or checking account17, putting it to work for you by buying I bonds is a good move.

Dealing with TreasuryDirect

The TreasuryDirect website is a bit of a pain to deal with as it’s old and finnicky.

I answered a security question incorrectly, then accidentally pressed the back button, and got locked out of my account.

For what it’s worth:

- Make sure to write down your answers in a secure place.

- Answers to security questions aren’t case sensitive.

- The TreasuryDirect customer service reps are helpful… once you’re able to reach them. I called when they open at 7 AM EST and was on hold until 7:45.

- Getting my account unlocked took about five minutes. I had to verify myself (head’s up, you’ll be asked for your account number and your driver’s license) and that was it.

Summary

Here’s the rundown on I bonds:

- I bonds are issued by the US government and are essentially risk-free.

- I bonds are tied to inflation, so when inflation is high, I bonds offer a high return.

- I bonds mature after 30 years.

- The interest rate of an I bond is the fixed rate plus the inflation rate.

- The fixed rate stays constant for the life of the bond.

- The inflation rate changes every May and November.

- The interest rate for an I bond will never go below zero.

- You can purchase I bonds through TreasuryDirect.gov.

- You can buy a minimum of $25 and a maximum of $10,000 worth of I bonds per person, per year.

- A business or trust can purchase another $10,000 and you can use your federal tax refund to purchase another $5,000.

- You cannot sell an I bond during the first year.

- If you sell an I bond within the first five years, you lose the last three months of interest.

- Interest on an I bond gets paid on the first of each month.

- An I bond’s interest compounds every six months.

- You only pay federal taxes on an I bond. There are no local or state taxes.

- The federal tax can be paid annually or deferred until you sell the bond or the bond matures.

There we go. Pretty much all there is to know about I bonds can be found in this post.

Next time I forget some detail, I know where to go. 😄

Stay in touch!

Enjoying so far? Get my posts delivered straight to your inbox each week. 📨

*If this form gives you any trouble, reach out to me at hi@pathtosimple.com and I’ll help you out.

Footnotes

-

See the Investor.gov website for the source of this quote. ↩

-

Buying a company’s stock, on the other hand, is fairly risky as the company might go out of business. In this case, you’d lose your money as the stock you own would be worthless.

There’s nearly 0% chance of this happening with a government bond as the US government is guaranteeing that they’ll pay you what they promised.

If the US starts defaulting on their debt, that’s the end for the world’s economy. ↩

-

See the I bonds interest rates page on TreasuryDirect. ↩

-

See this chart from TreasuryDirect which contains all I bond interest rates going back to 1998, which is when I bonds were first issued. ↩ ↩2

-

This isn’t exactly right because inflation is personal as not all goods and services are affected equally.

For example, if the cost of avocados increases by 20%, then an avocado fanatic will experience a high increase in their expenses while someone who doesn’t eat avocados (or is willing to do without them) won’t.

Similary, in a certain period, the price of gas might go up 10% while the price of milk goes down 5% and the price of electricity goes up 15%. Inflation might average out to 10%, but the inflation you experience would vary depending on the goods and services you buy.

So while inflation affects us all, the magnitude of the effect varies from person to person. ↩

-

0.001 + (2 × -0.0278) + (0.001 × -0.0278) = -0.0546

and -0.0546 × 100 = -5.46% ↩

-

See How To Predict I-Bond Savings Bond Rates by Jonathan from MyMoneyBlog. Jonathan also wrote a post on how to predict the I bonds rate for November 2022. ↩

-

287.504 - 274.310 = 13.194

13.194 ÷ 274.310 = 0.0481

0.0481 × 100 = 4.81%

You can use this percent change calculator to double check your math. ↩

-

Credit to the Bogleheads for this tip. ↩

-

See this page on TreasuryDirect for instructions on how to sell an I bond. ↩

-

From TreasuryDirect:

↩Note: For bonds less than 5 years old, values shown in TreasuryDirect and the Calculator don’t include the last 3 months of interest. That’s because if you cash a bond before 5 years, we don’t pay you the final 3 months of interest.

-

p is $10,000, r is 0.0712 (7.12%), n is 2, and t is (6-3)/12 since I’ve received 6 months of interest minus 3 months of “penalty”—since the bond is under five years old—and there are 12 months in a year.

So I’ve essentially received 3 months of interest, which makes t be 3 ÷ 12, or 0.25, which is a quarter of a year. ↩

-

$10,000 × (1 + 0.05/2)2 × 1 = $10,506.25 ↩

-

See the Bogleheads wiki to learn more about how this works. ↩

-

My mom does this.

She keeps her earnings in a savings or checking account—making nearly no interest—because she likes the availability as well as the “safety” (as opposed to the “riskiness” of the stock market).

I bonds, with their current high interest rates, are perfect for someone like my mom. ↩