Retirement plans come in two flavors:

- Defined benefit (DB) plans, a.k.a pensions

- Defined contribution (DC) plans, the most popular of which is the 401k1

We’ll cover both in detail below.

Pensions

Defined benefit plans are usually referred to as pensions.

With a pension, your employer promises to pay you a certain amount starting from the day you retire until the day you die.

How much you receive is based on an employer-defined formula generally involving:

- How long you worked at the company

- How much you were paid

The pension plan for public school teachers in Florida, for example, uses the following formula:

1.6% × Average of 8 years of highest salary × Years of service

So if a teacher:

- Reached a max salary of $50,000 (and maintained it for 8 years)

- Retired after 40 years on the job

Their annual payment would be $32,000 or $2,666.67 per month.2

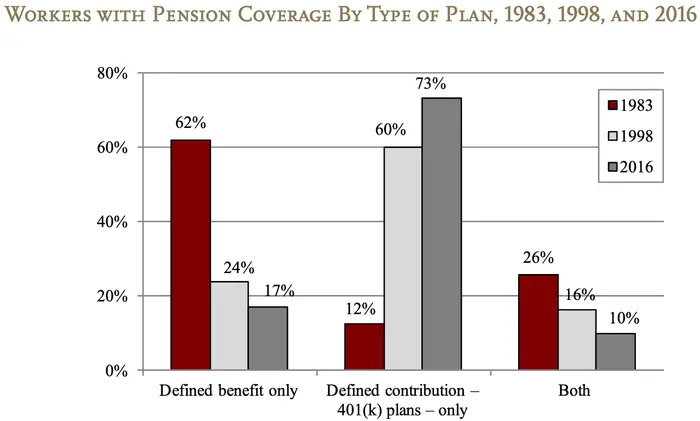

Pensions were common until the early 1980’s.

Chart courtesy of the Center For Retirement Research at Boston College.

Nowadays they’re exceedingly rare outside of the public sector (government jobs, teachers, policemen, firemen, etc.)

And even the public sector is trying to do away with them.

There are three main reasons for the decline of pensions:

- Employees have become more mobile

- It’s rare these days for someone to spend their whole working life in a single company.

- Since part of the formula is years of service, pensions don’t make as much sense as they used to.

- Pensions are expensive

- Companies don’t want to pay you for the rest of your life, especially with rising life expectancies. It’s a risk they’d rather avoid.

- The tax code was changed in 1978, bringing the 401k into existence

401k

A 401k is an example of a defined contribution plan and is the most commonly used retirement plan in the U.S.

In a defined contribution plan, you put a percentage of your paycheck into a retirement account provided by your employer.

You then choose how to invest this money to increase its growth.

Unlike with a pension, a defined contribution plan makes no guarantee of how much you’ll get paid upon retirement.

This amount wholly depends on how much you contributed into the account and how your investments fared.

Sidenote

A defined benefit (DB) plan derives its name from the fact that the benefit you’ll receive upon retirement, i.e. the monthly payments, is clearly defined.

Defined contribution (DC) plans, meanwhile, clearly define how much you can contribute, i.e. add to the account, but how much you get paid in retirement can fluctuate.

A 401k reduces risk for the employer as it doesn’t leave them on the hook for making monthly payments to you for the rest of your post-retirement life as pensions do.

This reduced risk for companies is another reason why pensions are rare and growing rarer.

Even in the public sector—the last stronghold of pensions—defined contribution plans are starting to pop up as an alternative to defined benefit plans.

So what are the benefits of a 401k?

- Free money

- A common perk of 401k plans is for an employer to match a percentage of your contributions.

- For example, an employer might offer a 3% match. This means they would match your contributions up to 3% of your salary.

- If your salary is $50,000, your employer match would max out at $1,500.3

- So if you contributed $1,500, your employer would match your contributions, and by the end of the year you’d have $3,000 in your 401k.

- Tax advantages

- Contributing to a 401k lowers your taxes.

- In the example above, by contributing $1,500 into your 401k, you’d only have to pay income tax on $48,5004 of your salary rather than on the full $50,000.

- The employer match doesn’t reduce your taxable income, unfortunately.

- You can invest your 401k contributions

- Investing your money can increase its growth and any investment gains are tax free.

- The only time you’ll pay taxes on your 401k is when you withdraw money from it in retirement.

Anything else worth knowing about the 401k?

Yes, two final things:

- You have to wait until you’re 59½ to start withdrawing money from your 401k

- If you withdraw money before then, you’ll be hit with a stiff 10% penalty.

- The government gives a tax break to incentivize people to save for retirement. This penalty is their way of ensuring that people actually use the money for retirement and not a 55-inch TV.

- There are a few exceptions to this rule that likely don’t apply to you.

- The 401k has an annual contribution limit

- In 2022, the 401k limit is $20,500, unless you’re 50 or older, in which case it’s $27,0005.

- The employer match doesn’t count towards the limit—you can contribute the full $20,500 AND get the employer match.

- This annual limit generally increases every year or every other year to account for inflation.

Summary

There you have it. You’re now well-versed in 401(k)s and pensions.

Become comfortable with the 401k because it’s a valuable tool in your personal finance toolbelt.

The free money from your employer, the tax advantages, and the investment growth of your contributions will snowball your 401k into a big win over the years.

I hope this was helpful. Shoot me an email if you have any questions.

And if you’re looking to learn more, you can check out the whole Personal Finance Basics Series.

Video for this post

If you prefer watching to reading, here’s an easy-to-follow video I made with all this info:

Slides for this post

If you’re interested, check out the slides I made for the video.

Stay in touch!

Enjoying so far? Get my posts delivered straight to your inbox each week. 📨

*If this form gives you any trouble, reach out to me at hi@pathtosimple.com and I’ll help you out.