In previous posts of the Personal Finance Basics series we covered:

- The pitfalls of investing in the stock market

- The stock market is a wealth-generating machine

- How to profit from the stock market

As a summary, we learned that:

- When we purchase shares of a company, we’re making a bet on that company’s future potential to grow and become more valuable.

- Companies, like humans, however, have a set lifespan. They’re born, they grow, and they die. No company, even the most successful and innovative, is eternal.

- It’s incredibly difficult to predict which companies will thrive and which will die.

- The decision to buy or sell stock of a specific company at a specific time is an attempt at predicting the future. And we’re terrible at predicting the future.1

- A mutual fund is a pool of money that’s managed by an investment company. The company takes in money from investors and uses it to buy shares of companies.

- An index fund is a type of mutual fund that tracks an index to decide which company’s stock to buy and in what proportion.

- An S&P 500 index fund buys shares in each of the 500 companies according to the market cap of each company.

In this post we’ll pick up where we left off and talk about how we can use index funds to tap into the stock market’s wealth-generating potential while limiting its dangers.

What is an index fund?

Let’s deconstruct a specific index fund to get a better idea of their inner workings.

We’ll use one of the most popular2: the Vanguard Total Stock Market Index Fund (better known as VTSAX).

What is VTSAX?

VTSAX stands for Vanguard Total Stock Market Index Fund.

Let’s break down this name into its components.

What does VTSAX stand for?

The V in VTSAX stands for Vanguard. Vanguard is the investment company that manages this index fund.

The TS stands for total stock market. This refers to the fact that this fund tracks the CRSP3 US Total Market Index.4

The A stands for admiral which is a term used by Vanguard to describe a class of shares that charge lower fees.

And the X indicates that it’s a mutual fund—all mutual fund stock symbols5 end with an X6.

Total stock market vs S&P 500

The CRSPTM and the S&P 500 are very similar, except for one major difference. And that is the number of companies tracked by each index.

CRSPTM includes around 4,000 companies compared to the 500 in the S&P 500.

This means that the CRSPTM tracks nearly 100% of US public companies7 while the S&P 500 only tracks 500 prominent ones.

The additional ~3,500 companies included in the CRSPTM add an extra bit of diversification.

Sidenote

CRSPTM is able to track more companies by including more stock exchanges.8

All well-known companies trade either on the NYSE or the NASDAQ. Smaller companies trade on other exchanges, like the NYSE American or the NYSE ARCA.

By way of analogy, a well-known brand is able to sell their products in Walmart. An unknown brand might sell on Etsy or their own website as these have lower (and cheaper) entry requirements.

Walmart and Etsy are analogous to the stock exchanges. Walmart (like the NYSE and NASDAQ) provides higher exposure and more prestige but is harder to get into.

And what’s the difference between the NYSE and the NASDAQ?

- The NYSE is older (founded in 1792 vs. 1971 for the NASDAQ) and generally regarded as more prestigious (due to its age and the high status of the companies listed on it.)

- The NASDAQ, meanwhile, has lower annual fees (companies have to pay to sell their stock on these exchanges) and lower entry requirements. This is why tech startups generally list on the NASDAQ over the NYSE.

Sorting the CRSPTM by market cap

We can run through the same exercise as in the last post to figure out what percent of CRSPTM’s total market cap each of the companies it tracks accounts for.

To do this, we’d need to:

- Sort the companies in the CRSPTM by their market cap.

- Divide the company’s market cap by the total market cap of CRSPTM.

Luckily for us, CRSP already provides this for us.

Sidenote

A company’s market cap is its market value, i.e., the amount of money it would take to purchase all of the company’s shares. It’s calculated by multiplying share price by shares outstanding.

If VTSAX uses the CRSPTM to decide how to allocate its funds, we would expect for the composition of VTSAX to be identical to that of CRSPTM.

And—spoiler alert—that’s exactly what we find.

Here’s how VTSAX and CRSPTM compared on June 30, 20229:

| Company | % of VTSAX | % of CRSPTM |

|---|---|---|

| Apple | 5.52% | 5.62% |

| Microsoft | 5.05% | 5.13% |

| 3.26% | 3.31% | |

| Amazon | 2.41% | 2.45% |

| Tesla | 1.56% | 1.58% |

| UnitedHealth Group | 1.27% | 1.29% |

| Berkshire Hathaway | 1.20% | 1.26% |

| Johnson & Johnson | 1.23% | 1.25% |

| 0.97% | 0.99% | |

| Exxon Mobil | 0.95% | 0.96% |

Almost identical.

In a perfect world, the composition of an index fund (VTSAX) would be exactly the same as that of the index it tracks (CRSPTM).

Slight deviations, however, are normal.10

Sidenote

The CRSPTM and the S&P 500 are examples of a capitalization-weighted index (or cap-weighted index for short). In a cap-weighted index, a company’s market cap is divided by the index’s total market cap to come up with the company’s weight in the index.

Because of this, companies with a higher market cap—Apple, Microsoft, Google, etc.—make up a larger percentage of the index than than those with a lower market cap—Under Armour, Alaska Air, etc.

The counterpart to a cap-weighted index is a price-weighted index, such as the Dow. In a price-weighted index, a company’s share price is divided by the sum of the share price of all the companies in the index to come up with the company’s weight in the index.

Because of this, companies with a higher stock price—UnitedHealth Group, Goldman Sachs, etc.—make up a larger percentage of the index than those with a lower stock price—Walgreens, Intel, etc.

What does it all mean?

Let’s recap what we’ve learned so far:

- VTSAX is an index fund which tracks the CRSPTM.

- The CRSPTM is very similar to the S&P 500. The main difference is that it includes more companies—about 3,500 more.

- The composition of VTSAX is nearly identical to that of the CRSPTM—as we would expect given that VTSAX tracks the CRSPTM.

This is all well and good, but what does it mean?

Let’s go through a step-by-step breakdown:

- You decide you want to start investing to profit from the long-term growth of the US stock market.

- Wanting to diversify your investment across all public US companies—an optimistic bet on the future of the US—you choose to buy VTSAX.

- Shares of VTSAX are trading at $100.11

- You invest $500. In exchange, you’re given 5 shares of VTSAX.

- VTSAX takes your $500 and invests it into each of the companies it tracks according to the company’s weight in the index.

- 5.52% of your $500—$26—goes to buying Apple stock.

- 5.05%—$25.25—goes to buying Microsoft stock.

- 3.26%—$16.30—goes to buying Google stock.

- And so on until your entire $500 have been allocated.

- By virtue of owning shares of VTSAX, you become a stockholder of Apple, Microsoft, Google, Amazon, Tesla, Nvidia, as well as 4,000+ other companies.

- When the prices of the companies tracked by VTSAX go up, VTSAX’s share price goes up. When the prices of these companies go down, VTSAX’s share price goes down.

It’s amazing how hard people make what is a simple game. But of course, if they told everybody what a simple game it was, 90% of the income of the people that were speaking [financial advisors] would disappear.

That’s it. It’s a simple game.

Sidenote

The total assets of a mutual fund are tallied at the end of each day. This is done by summing the market value of all the shares of the different companies that the mutual fund owns.

For example, if the mutual fund owns 10 shares of Company A whose stock price is at $20 and 20 shares of Company B whose stock price is at $30, the fund’s total assets on that day would be 10 × $20 + 20 × $30 = $200 + $600 = $800.

This number is divided by the total number of shares of the mutual fund in existence, i.e., shares outstanding, to come up with the mutual fund’s share price.

If the total assets came out to $300 billion and there were 3 billion shares outstanding of the mutual fund, the share price would be $100. This means it would cost you $100 to purchase one share of the mutual fund.

The next day, investors would buy shares of the mutual fund at $100 per share. If 100 shares were sold, the shares outstanding would increase by 100 and the $10,000 (100 shares × $100) would be used to purchase shares in companies according to the index.

At the end of the day, the total assets and shares outstanding would be computed again to determine the new share price. And so on, to infinity.

Beware of fees

By this point, we know that:

- Trying to pick specific companies or time the market is a fool’s game.

- An index fund, such as VTSAX, allows us to easily invest in all US public companies, providing great diversification.

The danger of betting on the wrong companies, however, isn’t the only pitfall we have to watch out for—there’s also the matter of high fees. 🤮

All mutual funds charge a fee to investors to account for the costs incurred in managing the fund—salaries to accountants and the fund’s managers, marketing expenses, office space, etc.

This annual fee is called the expense ratio of the fund and is expressed as a percentage.

For example, if you had $100,000 invested in a mutual fund with an expense ratio of 1%, you’d pay $1,000 a year in fees.

1% might not seem like much until you run the numbers. When you do, you’re in for a shock.

Let’s say you invested $25,000 and this money grew 7% per year for 40 years. At the end of the 40 years you’d have $374,361.45. Not too shabby.

Sidenote

The formula to calculate the growth of money is P × (1 + r)n, where P is the amount of money invested, r is the rate of growth, and n is the number of years. This is called the compound interest formula.

In our example, this would be $25,000 × (1 + .07)40, which equals $374,361.45.

What if the money grew at 6% instead? How much of a difference could the measly 1% make?

Take a guess.

With a growth rate of 6%, we’d end up with $257,142.95 after the 40 years.

That’s a loss of $117,218.50 due to the 1% fee. If that’s not absolutely bonkers, I don’t know what is.

The message here is that fees matter a whole lot.

What is a reasonable fee for an index fund?

An expense ratio under 0.10% is acceptable. Any other fees are unacceptable.

VTSAX, for example, has an expense ratio of 0.04% and no other fees.

In summary, look for index funds:

- With an expense ratio under 0.10%.

- With no extra fees.

- Some funds charge a fee when you buy or sell shares. Look for no-load funds to avoid these fees.

- Some funds also charge an annual account fee. Make sure the fund you pick doesn’t.

Passive vs active mutual funds

Are index funds the only type of mutual funds out there?

Not by a long shot.

Index funds are known as passively-managed funds.

The word passive comes from the fact that the components of the index fund—the companies it buys shares in—are determined by the index being tracked rather than by a person.

The components of an S&P 500 index fund, for example, are determined by the composition of the S&P 500.

If Apple’s market cap accounts for 6% of the S&P 500’s total market cap, then Apple will account for 6% of the assets of an S&P 500 index fund. Out of every dollar added to the index fund, 6 cents will go towards buying Apple stock.

Robot-like precision without human intervention.

The counterpart to passively-managed funds are actively-managed mutual funds.

The word active comes from the fact that the components of the fund are determined by the fund manager.

If the fund manager is a big believer in Tesla, for example, she’ll purchase more shares of Tesla than of other companies. This could lead to Tesla accounting for 20% (or 30% or 50%, etc.) of the fund’s assets compared to the 1.97% in VTSAX.

The composition of an actively-managed fund will reflect the bets and beliefs of the fund manager rather than any index.

Sidenote

ARK Innovation is an example of an actively-managed mutual fund. You can check out it’s holdings and compare them to those in VTSAX.

You’ll see that in ARK—as of September 13, 2022—Tesla and Zoom have a weight of 9.66% and 7.7%, respectively. In VTSAX, meanwhile, Tesla and Zoom have a weight of 1.89% and 0.05%.

This is a huge difference. Investing in ARK is riskier because it’s betting big on two companies. If Zoom and Tesla do well, ARK will experience higher growth than VTSAX. If they don’t, VTSAX will trounce it.

Which should we go with?

There are two factors to consider when deciding between an active and a passive mutual fund: growth and fees.

We want growth to be as high as possible and fees to be as low as possible.

So how do active and passive mutual funds compare in these two dimensions?

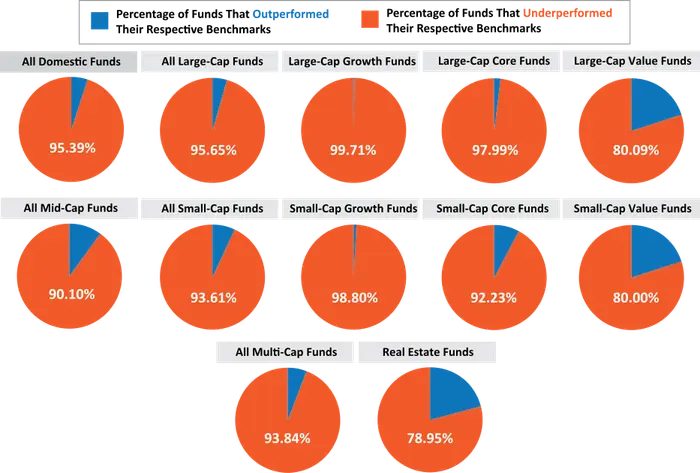

- Growth: 95% of active mutual funds that invest in US companies underperformed their passive counterparts.

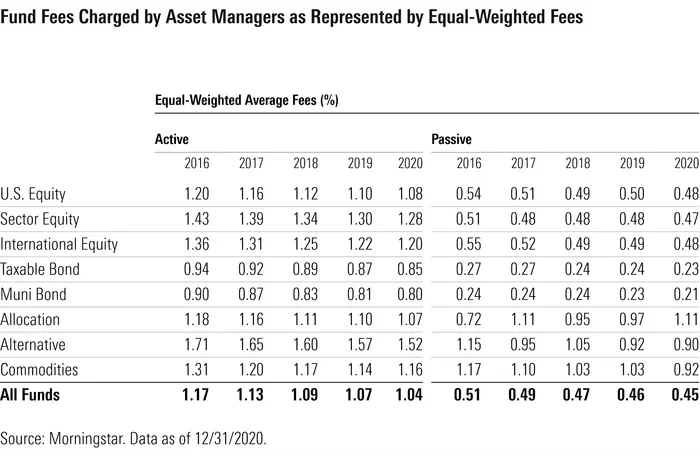

- Fees: the average expense ratio for active mutual funds was 1.08%. It was 0.48% for their passive counterparts. That’s more than twice as high.

These two charts say it all:

Chart courtesy of IFA. Note how much bigger the orange slices—passive funds—are than the blue slices—active funds.

Chart courtesy of Morningstar. Note how much lower the fees are for passive mutual funds across all the different categories.

Lower growth and higher fees so that fund managers can laugh their way to the bank? Count me out.

Summary

In this post we learned that:

- VTSAX is a popular total stock market index fund.

- It’s managed by Vanguard and invests in over 4,000 public companies in the US.

- It tracks CRSPTM, which is a cap-weighted index. As a result, VTSAX holds a higher percentage of its money in companies with a higher market cap.

- For example, VTSAX holds 10 times more money in Apple stock than in Bank of America stock as Apple’s market cap is 10 times higher than Bank of America’s.

- Index funds are passively-managed mutual funds.

- Index funds seek to replicate the performance of the index they track (though there’s always a small tracking error.)

- If the S&P 500 grows by 10%, then an index fund tracking the S&P 500 will grow by 10%.

- There also exist actively-managed mutual funds.

- Actively-managed funds rely on the analysis and intuition of the fund’s manager.

- The fund manager decides in which companies to invest and what each company’s weight should be.

- The fund’s performance depends on the bets made by the manager. There’s no correlation with an index as in the case of index funds.

- Fees are a huge drag on performance.

- A 1% fee on a $25,000 investment will cost us $117,218.50 over a 40-year period, assuming 7% vs. 6% growth.

- We should make sure that the fund’s expense ratio is under 0.10% and that it has no other fees.

- Index funds are valuable tools because they:

- Provide diversification as we’re investing in hundreds of quality companies.

- Save us the work of having to individually buy stock in each of these companies.

- Have lower fees and higher growth than active mutual funds.

In the next post, we’ll take a second to breathe and review everything we’ve learned about the stock market and investing.

After that, we’ll look at how to open an investing account and buy our first shares of an index fund.

I hope this was helpful. Feel free to send me an email if you have any questions.

And if you’re looking to learn more, you can check out the whole Personal Finance Basics Series.

Slides for this post

If you’re interested, check out the slides I made for this post.

Stay in touch!

Enjoying so far? Get my posts delivered straight to your inbox each week. 📨

*If this form gives you any trouble, reach out to me at hi@pathtosimple.com and I’ll help you out.

Footnotes

-

Based on the amount of money invested in the fund. See Wikipedia for a ranking of US mutual funds by assets under management. ↩

-

CRSP stands for Center for Research in Security Prices. It’s a subsidiary of the University of Chicago that does research into investing and the stock market. They also manage their own stock market indices, such as the CRSP US Total Market Index. ↩

-

Vanguard also offers an index fund (VFIAX) that tracks the S&P 500 instead of the total stock market. ↩

-

A stock symbol is the shortcode assigned to public companies. The stock symbol for Amazon, for example, is AMZN. For Apple, it’s AAPL. And for Tesla, it’s TSLA. Check out Investopedia for more examples. ↩

-

This allows investors to easily determine what the stock symbol represents: a company (like Apple), a mutual fund, or some other type of fund. Check out Investopedia for more context. ↩

-

You can read this PDF if you’re curious about the exact methodology CRSP uses to decide whether to include a company in CRSPTM. ↩

-

The S&P 500 only includes companies traded on the NYSE, NASDAQ, and BZX Exchange. CRSPTM also includes companies traded on the NYSE American, NYSE ARCA, and the Investors Exchange.

The exchanges included in the S&P 500 are listed in the info box in Wikipedia. For CRSPTM, see their quarterly report. ↩

-

CRSP updates the CRSPTM report once a quarter—at the end of March, June, September, and December. ↩

-

This deviation is called a tracking error. ↩

-

The actual price of a share of VTSAX varies from day to day, of course. You can see the current price on Vanguard. ↩