In the previous Personal Finance Basics post we covered IRAs.

In this post we’ll cover the Roth IRA, which is just a variation of the Individual Retirement Account (IRA).1

IRAs

Let’s quickly recap IRAs.

IRAs have:

- An annual contribution limit

- Restrictions on when you can withdraw your money

- You must be 59½ to withdraw money from an IRA or you’ll pay a 10% penalty tax.

- There are some exceptions to this restriction.

- The two most common ones are using you IRA to pay for higher education (tuition, books, etc,) and using up to $10,000 to purchase a house.

- Income restrictions

- You can only contribute to an IRA if your annual income is below the IRS-defined threshold.

- The threshold varies depending on:

- Whether you’re covered by a retirement plan at work

- Whether you’re single or married

- Your annual income

- Tax advantages

- Contributing to an IRA reduces your taxes by reducing your taxable income.

- You don’t pay any tax on money you add into an IRA. It’s as if you’re putting a spell on the IRS, “This is not the money you are looking for.”

How are Roth IRAs different?

Let’s take a look at these four dimensions to see how Roth IRAs differ from traditional IRAs.

Annual contribution limit

The annual contribution limit is exactly the same for Roth and traditional IRAs.3

Note that this limit applies across IRAs, both traditional and Roth.

In other words, it’s not $6,000 for your traditional IRA and another $6,000 for your Roth IRA—it’s $6,000 across both.

You can use 100% of the limit on your traditional or Roth IRA or you can split the limit between them in whatever proportion you choose.

Restrictions on withdrawals

The withdrawal restrictions on Roth IRAs are slightly different than on traditional IRAs.

One thing we didn’t touch on in the last post is that there are two parts to an IRA:

- Your contributions

- The earnings on your contributions

Say Fred puts $6,000 into his Roth IRA in 2022 and invests this money into the stock market.

Fred forgets about his Roth IRA and doesn’t make any further contributions for the next few years.

The stock market increases in that time and by 2025 Fred’s $6,000 have grown to $6,500.

Fred now has $6,000 worth of contributions in his Roth IRA and $500 worth of earnings.

Unlike in a traditional IRA, the $6,000 of contributions have no restrictions. Fred can withdraw this money whenever he wants without any penalty.

The $500 in earnings, however, have similar restrictions to those of a traditional IRA.

If Fred wants to avoid the 10% penalty when withdrawing earnings from his Roth IRA, he’ll need to:

- Have held the Roth IRA for at least five years4

- Be 59½ or older

This means Fred wouldn’t be able to access his Roth IRA earnings until 2027, at the earliest.

As with traditional IRAs, there are some exceptions.

But the advice I gave for traditional IRAs applies for Roth IRAs too—don’t make early withdrawals and allow your IRA to grow uninterrupted for as long as possible.

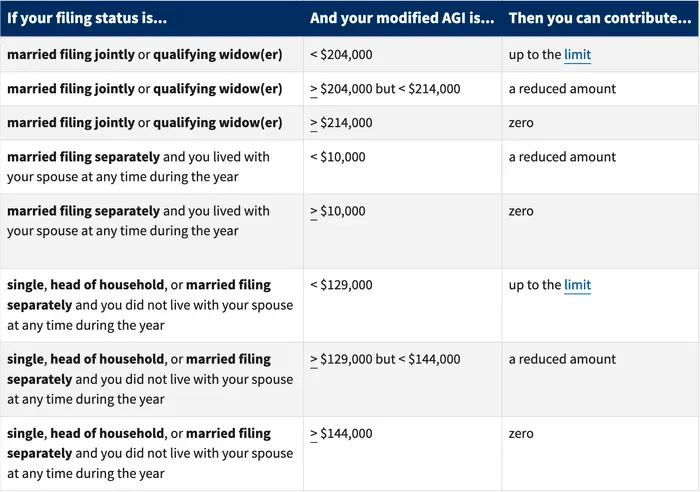

Restrictions on income

The only difference in income restrictions between the Roth IRA and the traditional IRA is that the limit is higher for the Roth IRA.

Here’s the full table that covers how much you can contribute to a Roth IRA in 2022 depending on your filing status (single vs married) and your income:

Table courtesy of the IRS.

As we covered in the previous post, your modified AGI is your annual income minus some deductions (e.g., 401k contributions).

But don’t worry because we’ll cover AGI and modified AGI in more detail in a later post.

Tax advantages

The difference in tax advantage between the traditional IRA and the Roth IRA is the biggest differentiator between them.

As an example, Alice makes $60,000 in 2022 and contributes the $6,000 maximum to her IRA.

This contribution lowers her taxable income from $60,000 to $54,000, so she’ll pay income taxes as if she had made $54,00 rather than $60,000.

When Alice turns 59½ and goes make a withdrawal from her IRA, however, she’ll have to pay income tax on the withdrawal as she hadn’t paid taxes on this money before.5

(Whether on the way in or on the way out, Uncle Sam always gets you 😉)

What if Alice decides to contribute the $6,000 into a Roth IRA instead?

This contribution will not lower her taxable income. In the eyes of the IRS, her income remains $60,000.

When Alice turns 59½ and goes to make a withdrawal from her Roth IRA, however, she’ll pay no taxes!6

Alice’s Roth IRA will grow and grow during her working years and in retirement she’ll get to make tax-free withdrawals as she has already paid taxes on this money.

This is the big tax advantage of the Roth IRA.

To sum up:

- The traditional IRA gives you a tax advantage now by reducing your taxable income and thus reducing your income tax for that year.

- The Roth IRA gives you a tax advantage in the future as you’ll never again have to pay taxes on this money.

Should I use a Roth IRA or a traditional IRA?

If your income allows you to contribute to a traditional IRA, you should do that.7

If your income is too high for the traditional IRA, you should contribute to a Roth IRA.8

Combining these two strategies means you’ll likely start your working years by contributing to an IRA and then hopefully (after some raises) switch and start contributing to a Roth IRA.

What if I make too much even for a Roth IRA?

If your income is too high to contribute even to a Roth IRA, good on you!

As luck would have it, you can still contribute to a Roth IRA through what’s called a Backdoor Roth IRA.

We’ll cover this in an upcoming post.

Summary

There you have it. You’re now well-versed in Roth IRAs.

Become comfortable with the Roth IRA because it’s a valuable tool in your personal finance toolbelt.

Maxing out and investing your contributions, along with the tax advantages, will snowball your Roth IRA into a big win over the years.

I hope this was helpful. Shoot me an email if you have any questions.

And if you’re looking to learn more, you can check out the whole Personal Finance Basics Series.

Video for this post

If you prefer watching to reading, here’s an easy-to-follow video I made with all this info:

Slides for this post

If you’re interested, check out the slides I made for the video.

Stay in touch!

Enjoying so far? Get my posts delivered straight to your inbox each week. 📨

*If this form gives you any trouble, reach out to me at hi@pathtosimple.com and I’ll help you out.

Footnotes

-

The Roth IRA is named for William Roth, a senator from Delaware, who sponsored the Taxpayer Relief Act of 1997 which created the Roth IRA. ↩

-

As we learned in the previous post on IRAs, workers over 50 get to make catch-up contributions to set more money aside for their incoming retirement. ↩

-

Non-Roth IRAs are referred to as traditional IRAs. ↩

-

This is known as the Roth IRA five-year rule. ↩

-

With a traditional IRA you’re essentially deferring when you pay income taxes.

In other words, you’re choosing to pay them later on when you make withdrawals in retirement rather than now.

This can be very beneficial as your income is likely to be lower in retirement meaning you’ll pay less taxes. We’ll cover this more in a future post. ↩

-

With a Roth IRA you do the opposite: you pay taxes now instead of paying them later. ↩

-

Remember that your 401K contributions lower your modified AGI (MAGI).

If you contribute the max to your 401K ($20,500 in 2022) your income can be as high as $88,500 ($68,000 IRA income limit in 2022 + $20,500) and you’ll still be eligible to contribute to an IRA. ↩

-

If you contribute the max to your 401K, you can make up to $149,500 ($129,000 Roth IRA income limit in 2022 + $20,500) and still be eligible to contribute to a Roth IRA. ↩