In the previous Personal Finance Basics post we covered 401(k)s and pensions.

In this post, we’ll cover Individual Retirement Accounts (IRA), which, like a 401k, can help reduce your taxes.

Individual Retirement Accounts

An IRA (short for Individual Retirement Account) is another retirement plan available in the U.S.

An IRA is similar to a 401k. They both:

- Have tax advantages

- Contributing to an IRA reduces your taxes by reducing your taxable income.

- If you make $50,000 and put $3,000 into your IRA, you’ll only pay income tax on $47,0001 rather than on the full $50,000.

- Can be invested

- Investing your money can increase its growth and any investment gains are tax-free.

- You don’t pay taxes on the money you add to your IRA and you don’t pay any taxes on it while it’s inside the IRA.

- The only time you’ll pay taxes on this money is when you withdraw it from the IRA in retirement.

- Have an annual contribution limit

- The annual limit for 401(k)s is straightforward—it’s $20,500 (in 2022) unless you’re 50 or older, in which case it’s $27,000.2

- The annual limit for an IRA is slightly more complicated as it varies depending on:

- Whether you’re covered by a retirement plan at work (such as a 401k)

- Whether you’re single or married

- Your income

- Can’t be withdrawn until you’re 59½

- If you make a withdrawal before this, you’ll be hit with a 10% penalty tax.

- There are a few exceptions to this rule. These exceptions include:

- Paying for higher education (e.g., tuition, books, fees, etc.)

- Using up to $10,000 (lifetime limit) to buy a house, assuming you haven’t bought one within the past two years

- I wouldn’t recommend using your IRA funds for higher education or a house—let this money grow uninterrupted for as long as possible.

How is the limit calculated?

The annual limit is $6,000 if you’re under 50 and $7,000 if you’re 50 or older.3

If you’re not covered by a retirement plan at work, such as a 401k, you’re in the clear. You can contribute the full amount.

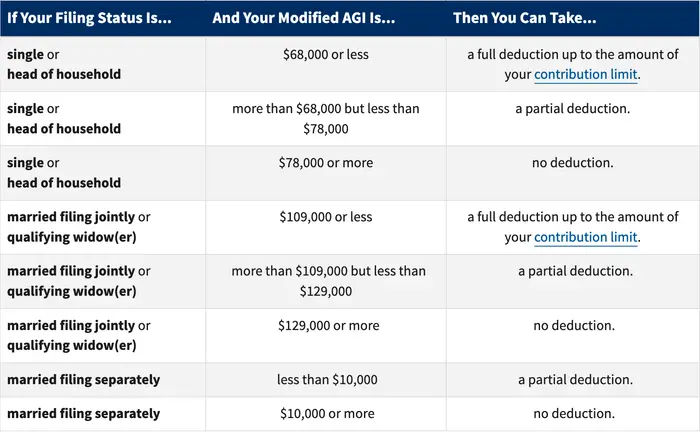

If you are covered by a retirement plan, you’ll need to refer to the table below.

Table courtesy of the IRS.

Looking at the table, we can see that if you’re single4 and your modified Adjusted Gross Income (AGI) is $68,000 or less, you’re in the clear. You can contribute the full amount.

What is your modified AGI?

Well, Gross Income (GI) is all the money you made in a year. It’s your salary along with any extra money you might’ve made such as interest on a savings account or a side hustle.

From your gross income you subtract some deductions, such as your contributions to a 401k, to get your Adjusted Gross Income5.

Then to get your Modified AGI, you add some of the deductions back in.

Don’t worry—we’ll cover AGI and modified AGI in more detail in a later post.

So if:

- You’re single

- Your gross income is $74,000

- You contribute $6,000 to your 401k

Then your modified AGI is $68,0006 and you’re in the clear to contribute the full amount to your IRA.

This is a key point: by contributing to a 401k you can lower your modified AGI and allow yourself to take advantage of making a full contribution to an IRA.

How is an IRA different from a 401k?

The main difference between an IRA and a 401k, aside from the different annual limit for each, is that you don’t need an employer to open up an IRA.

A 401k is a “perk” that an employer offers—you need an employer to be able to have a 401k7.

This means that your employer won’t match your contributions to your IRA as they do with your 401k.

Summary

There you have it. You’re now well-versed in IRAs.

Become comfortable with the IRA because it’s a valuable tool in your personal finance toolbelt.

Maxing out and investing your contributions, along with the tax advantages, will snowball your IRA into a big win over the years.

I hope this was helpful. Send me an email if you have any questions.

And if you’re looking to learn more, you can check out the whole Personal Finance Basics Series.

Video for this post

If you prefer watching to reading, here’s an easy-to-follow video I made with all this info:

Slides for this post

If you’re interested, check out the slides I made for the video.

Stay in touch!

Enjoying so far? Get my posts delivered straight to your inbox each week. 📨

*If this form gives you any trouble, reach out to me at hi@pathtosimple.com and I’ll help you out.

Footnotes

-

$50,000 - $3,000 = $47,000 ↩

-

Workers over 50 get to make catch-up contributions. This allows older workers to set more money aside for retirement. ↩

-

Another example of a catch-up contribution. ↩

-

You’re either single or married as far as taxes go. “Single” here just means you aren’t married. ↩

-

If your gross income is $50,000 and you contribute $10,000 to your 401k, your AGI is $40,000. ↩

-

$74,000 - $6,000 = $68,000 ↩

-

You can also open up a solo 401k if you’re self-employed with no full-time employees. It gets more difficult once you have employees. ↩