In the previous posts of the Personal Finance Basics series, we covered:

- How will I know when I’ve saved enough to retire?

- 401(k)s and pensions

- IRAs (Individual Retirement Accounts)

- Roth IRAs

- How Taxes Work

- Backdoor Roth IRA

- Health Savings Account (HSA)

- Adjusted Gross Income and Modified Adjusted Gross Income

Each of these posts built on one another and we now have a solid foundation of personal finance knowledge.

In this post, we’ll review everything we’ve learned so far.

4% Rule

How much money do I need to retire?

Ask 10 people this question and you’ll get 11 different answers.

One answer, backed by the Trinity Study, is to calculate your annual expenses and multiply this number by 25.

This sum of money should last you 30+ years, assuming you don’t increase your annual spending.

Why do we multiply by 25?

Because the finding of the Trinity Study was that a retiree can withdraw 4% of their portfolio every year and not run out of money. 100% divided by 4% is 25.1

So if you want to live on $40,000 per year, you’ll need $40,000 times 25 or one million dollars.

Amass these one million dollars and you’re financially independent.

This means you don’t have to earn another penny for the rest of your life as you can ride out your savings.

That’s the theory, anyway.

But it’s a whole different ballgame retiring at 35 than at 65. Not to mention that life has a way of pelting us with curveballs.

For early retirees, a 3.5% withdrawal rate—instead of the 4% suggested in the Trinity Study—is needed to ensure success.

This turns the 25x rule into the 28.6x rule.

With annual expenses of $40,000, you now need an extra $144,000—$1.144 million in total instead of $1 million—to be financially independent.

401k vs IRA vs HSA

What do 401(k)s, IRAs (traditional and Roth), and HSAs have in common?

- Tax advantages

- A 401k, a traditional IRA, and an HSA lower your income tax by reducing your taxable income.

- A Roth IRA doesn’t reduce your taxable income. However, you won’t pay taxes when making withdrawals from your Roth IRA in retirement.

- Employers might contribute money into your account

- This is generally the case with the 401(k) match and with HSAs.

- Yay! Free money.

- Age restrictions on when you can withdraw your money. You must be:

- 59½ to withdraw from your 401k or IRA.

- 65 to withdraw from your HSA for non-medical expenses, but you can make withdrawals for medical expenses at any time.

- The penalty for early withdrawals for the 401k and IRA is 10%; for the HSA it’s 20%.

- Annual contribution limits. In 2022, these limits are:

- Additional restrictions

- IRAs, both traditional and Roth, have income limits, though we can get around the Roth IRA income limit by using the Backdoor Roth maneuver.4

- Having an HSA is only possible if you have a high-deductible health plan (HDHP).

We can sum up the above as follows:

- Tax advantages and free money

- Restrictions (on withdrawals, annual contributions, income, etc.)

Flow of money

Given the above, we can describe these accounts with the following diagrams.

Accounts with tax-free contributions

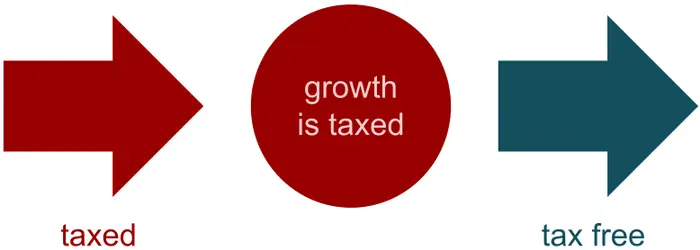

401(k)s, traditional IRAs, and HSAs have tax-free contributions, but we pay tax when we make withdrawals:

Note that we also don’t pay taxes on any investment gains5 we make along the way.

Accounts with tax-free withdrawals

Roth IRA contributions aren’t tax-free, but we never pay taxes on this money again:

Note that, as with tax-free contribution accounts, we don’t pay taxes on any investment gains we make along the way.

Standard investment account

For comparison, here’s what our investments would look like without these accounts:

Like with the Roth IRA, our contributions aren’t tax-free.

Bummer.

Unlike the Roth IRA and the tax-free contribution accounts, we also get taxed on our investment gains along the way.

Double bummer.

However, this account has no restrictions: no income or annual contribution limits and no age mandates preventing us from withdrawing our money whenever we want.

Silver lining.

We’ll cover the standard investment account in more detail in later posts.

Taxes

To calculate our annual income tax, we start with our gross income, which is the total sum of money we made in the year.

We then subtract contributions to a:

- traditional IRA6

- 401k

- HSA

- plus other deductions, such as student loan interest or the Educator Expense Deduction if you’re a teacher

to arrive at our Adjusted Gross Income (AGI).

Adjusted Gross Income = Gross Income - Deductions (“Adjustments”)

From our AGI we subtract the standard deduction to arrive at our taxable income.

Taxable Income = AGI - Standard Deduction

We then use the income tax brackets to determine exactly how much we’ll pay in taxes based on our income.

As we’ve mentioned, some accounts, like the traditional IRA and the Roth IRA, have an income limit.

This means that if you make more than $X, you can’t take the deduction for your contribution to a traditional IRA. And if you make more than $Y, you can’t contribute to a Roth IRA.

$X and $Y are determined annually by the Internal Revenue Service (IRS).

For example, the IRS will say:

In 2022, if you’re single, you can only deduct your contribution to a traditional IRA if your Modified Adjusted Gross Income is $68,000 or less.

How do we calculate Modified Adjusted Gross Income (MAGI)?

We take our Adjusted Gross Income and add some of the deductions we took back in.

Modified Adjusted Gross Income = AGI + some deductions

We add back in our deductions for our contributions to a traditional IRA and any student loan interest, along with a few others.

As a quick example, if our gross income is $67,000 and we contribute $6,000 to our traditional IRA and $2,000 to our HSA, our:

- AGI is $59,000 ($67,000 - $6,000 - $2,000)

- Taxable income is $46,050 ($59,000 - the standard deduction of $12,950)

- MAGI is $65,000 ($59,000 + $6,000)

See the post on how taxes work for more examples.

Plan of attack

Every dollar we can keep away from Uncle Sam’s grubby paws is a dollar we can put to work for ourselves.

Three key points to remember:

- The contribution limits for our 401K, IRA, and HSA reset every year.

- To derive the maximum benefit, we should max out our contributions to each of these accounts.

- How do we pick between the traditional and the Roth IRA?

- Use a traditional IRA if you’re able to deduct your contribution and lower your taxes

- Use a Roth IRA if your income is too high for a traditional IRA

- Use the Backdoor Roth if your income is too high for the Roth IRA

Summary

At this point, you should feel comfortable explaining:

- The 4% rule

- 401(k)s, IRAs (traditional and Roth), the Backdoor Roth, and HSAs

- How to calculate your income tax

to your dad, mom, five-year-old sibling, partner, best friend, enemy, or a random person on the street.

Sidenote

In fact, it would be a great test of your knowledge to go ahead and do this and see how you do!

Take some time to go back through the earlier posts in the series and review whatever is still hazy. If any doubts remain, feel free to send me an email with questions.

As always, I hope this was helpful.

And if you’re looking to learn more, you can check out the whole Personal Finance Basics Series.

Video for this post

If you prefer watching to reading, here’s an easy-to-follow video I made with all this info:

Slides for this post

If you’re interested, check out the slides I made for the video.

Stay in touch!

Enjoying so far? Get my posts delivered straight to your inbox each week. 📨

*If this form gives you any trouble, reach out to me at hi@pathtosimple.com and I’ll help you out.

Footnotes

-

The 4% rule and the 25x rule are two sides of the same coin. ↩

-

This limit applies across all IRAs (traditional and Roth)—you can’t contribute $6,000 to each. ↩

-

The limit is doubled for families. ↩

-

There’s no income limit to contribute to a traditional IRA. There’s only an income limit if we want to take the tax deduction for our traditional IRA contribution. ↩

-

If you buy a stock for $10 and sell it for $20, that’s a $10 investment gain.

Another possible gain is if the stock pays a dividend. Say you own a share of Apple and Apple decides to pay a dividend of $1 per share. That’s a $1 investment gain.

These investment gains aren’t taxed in tax-advantaged accounts like the 401K, IRA, and HSA. They are taxed in standard investment accounts. ↩